|

|

|

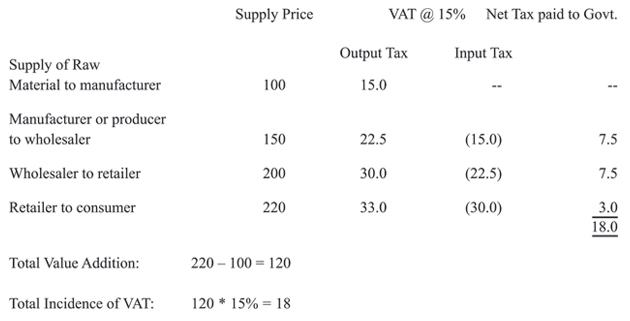

Sales Tax” is not a new term in Pakistan and has its roots in independence. In 1948, sales tax was levied under the Sales Tax Act, 1948. In 1951, a new Sales Tax Act was enacted and in 1990 yet another Sales Tax Act came into effect (1990 Act). Although in common parlance the 1990 Act is thought to be a levy of the general sales tax (GST), this is a misnomer as the term GST suggests a levy on sales. On the contrary, the effect of the 1990 Act is that it levies a value added tax i.e., VAT. Whilst occupying the field for over 20 years, the 1990 Act has witnessed several changes in the shape of the Provincial Sales Tax Acts/Ordinances and the subordinate rules and regulations made thereunder. Other legislative amendments include (i) introduction of federal excise duty being collected in ‘VAT mode’ on certain services, (ii) a long list of exemptions, (iii) a multiplicity of rates varying across industries or products, (iv) services sector largely being out of the ambit of sales tax net, (v) the concept of withholding tax and (vi) presumptive tax. All these additions have gradually crept in the sales tax regime and it is submitted that these alterations have the masked true intent behind the 1990 Act. In the above background and prompted by the Government’s requirement of achieving IMF’s performance criteria, revamping the 1990 Act came as a matter of necessity. This revision in the sales tax regime, though motivated by the IMF, may bring back the true spirit of the VAT. Recently, in February 2010, the Government has introduced before the Parliament the Bill, Federal Value Added Tax Act, 2010 (Federal Bill) and before the Provincial Assemblies the Provincial Value Added Tax Act, 2010 (Provincial Bills), which is intended to be introduced through the Finance Act, 2010. To appreciate the essence of the Federal and Provincial Bills, it is important to understand the concept of VAT, which may be understood with reference to the following illustration: Thus, the net revenue generated by the Government is the tax applied on the value addition accrued throughout the process. It would therefore follow that any exemption of the kind discussed above would distort the entire process and defeat the concept of VAT.

Some of the encouraging features of the Federal Bill and the Provincial Bills as compared to the 1990 Act are as follows:

Despite the above positive features there are many pitfalls, some of which are discussed below: • First of all the inflationary trend that VAT is going to initiate can be any one’s guess given that the ultimate burden of VAT is going to be on the consumers. If there is no relief for consumers from alternate appropriate measures (i.e. increase in wages or subsidies for essential commodities) by the Government then inflation induced by VAT would be devastating. • In spite of curbing the loops to ensure no breaking of the supply chain, some areas have remained unattended. One such area is the threshold of Rs. 7.5 million turnover for mandatory registration under VAT. Based on past experience and the tax-averse culture of our country, this will inevitably inspire a change of name (multiple entities) once any business concern reaches the threshold limit so as to avoid the further incidence of registration. • Value of imported goods is proposed to be extended to include actual service charges at the import stage, which is likely to lead to complications and claims. • Cross adjustment of VAT (input and output) on entities providing goods and services have not been provided for and is likely to cause hardships for the registered persons. • High level of protection to officers of Federal Board of Revenue (FBR). There is a bar on suits which provides that no suit maybe brought in any court including the High Courts to set aside or modify any order passed, assessment made, tax levied, penalty imposed etc. • The traditional protections afforded to limited liability companies is proposed to be abolished in the case of private limited companies by permitting recovery of tax liability of such companies detected before or after liquidation of the companies. • The Provincial VAT is proposed to be collected in the same manner as Federal VAT. It is apprehended that this will lead to disputes between the Federal and the Provincial Governments. As is currently being reported in the media, various trade bodies, associations and stakeholders who are already facing immense problems from the existing power crisis and the increasing cost of doing business have expressed their reservations and their intention to resist any move to enforce the VAT.1 1 Readers are also encouraged to review the Frequently Asked Questions (FAQs) on VAT issued by Federal Board of Revenue on 12.4.2010. The author is the Chief Financial Officer and Company Secretary at DHL Pakistan. Comments may be directed to editors@counselpakistan.com. | |

• Single tax rate at 15%. However proposals for charging 5-6% on the supply of consumer items which were previously charged on the basis of printed retail price are also under consideration, and being introduced largely for inflationary reasons;

• Single tax rate at 15%. However proposals for charging 5-6% on the supply of consumer items which were previously charged on the basis of printed retail price are also under consideration, and being introduced largely for inflationary reasons;Associate, Michelmores LLP, UK

OF THE SUBCONTINENT

Senior Associate, Orr, Dignam & Co.

Director, Atlas Asset Management Limited

Barrister-at-Law and an Advocate

of the High Courts

Director & General Counsel, Pfizer Laboratories

ITS CITIZENS

Head, Corporate and FI Origination,

Royal Bank of Scotland